Are you thinking about starting a p2p lending business? Then we have some good news. Starting a p2p lending business is much easier than starting a digital bank. To help you out, here is your ultimate guide to a p2p lending business launch with lots of development and marketing tips inside.

Reasons to Start a P2P Lending Platform

The P2P lending market is expected to reach one trillion issued loans by 2025. And this is not the only reason to create a peer-to-peer lending platform.

This business is quite trendy

Traditional financial institutions are too heavy and full of bureaucratic red tape. On the one hand, this is their way of protecting their investments. Still, this is additional time for ordinary users, mountains of unnecessary paperwork, and a lot of stress in obtaining a loan. Landing platforms offer a simplified alternative, allowing investors to make money out of money and borrowers to get a loan for their needs following a more simplified procedure.

P2P lending is the way to meet the demands of modern borrowers

What is more, p2p lending companies are a perfect match for Millenials. They find it quite profitable to become a p2p investor since this business model fits their worldview. They don’t like their time wasted and don’t like red tape but want a simple and safe solution to make their money work. According to research published by MoneyControl, 80% of p2p borrowers are young people (under the age of 35). This means that it will not be difficult to attract Millennials to the platform. The only thing you need is to carefully segment them into investors and borrowers and develop two different marketing strategies.

You don’t have to lend or risk your own money

You don’t need to have significant authorized capital to start a p2p lending business. Depending on the niche you choose, you will need an amount to cover the first three-five loans, and then, you will be able to reinvest your money again and again, plus attract other investors.

P2p Lending Platform Types, Niches, and Business Models

Despite all the seeming novelty of the concept and a significant decrease in banks’ influence against the background of the development of cryptocurrencies, p2p lending is not yesterday’s invention.

According to the Peer-to-Peer Lending: Business Model Analysis research, “Peer-to-peer lending communities can be traced back to 1630s and 1640s, years in which were first born the so-called Friendly Societies in Britain. These organizations featured many of the characteristics of the contemporary peer-to-peer lending communities. Upon registration, these societies granted privileges to its individuals, which often translated into mutual support and financial assistance.”

The possibility of building a p2p lending platform and making it fully digital and tech-driven opens up a lot of new opportunities. That is why certain p2p lending websites operate within a particular niche, welcoming a specific group of borrowers while still offering favorable conditions for investors. Here are the main p2p lending niches.

Education financing

There are 45 million students in America who have to pay off debts for their education. P2P lending can become a great alternative, even though many federal programs for college and university education provide financing, and banks themselves develop personalized loan products. With a specific p2p lending platform, it becomes easier to get a loan on better terms. What is more, this approach fits the worldview of modern young people, as we’ve already stated. Also, debt consolidation p2p platforms may be helpful for students already drowning in debts.

Car and real estate financing

The essence of the car financing p2p platform is also quite obvious. The finances raised from several investors can be rented out to a borrower to help him/her with purchasing a car. However, when developing such a platform, you need to carefully think about the mechanism for proving the borrower’s real solvency and goal. The same goes for real estate lending.

Business loans

In the case of business loans, it makes more sense to talk about b2b loans. However, the business model’s essence is still the same - companies and/or individuals rent out their money to a company/startup. Yet, investors’ only interest is to get their money back with an additional profit. They don’t want to have a share in the business of the borrower.

Medical treatment financing

With p2p lending software, it is also easier to get a loan for medical treatment. However, you need to protect the medical information you ask for carefully. It is very sensitive and expensive on the black market. So, in this case, you will need to invest in additional data protection tools. Otherwise, there is a tremendous reputational risk if the borrower’s medical data becomes available to third parties.

Microloans

This is the simplest example of p2p lending software. In this case, there will be modest sums of loans, plus the borrower, as a rule, has the right to spend the borrowed money any way they consider right. Also, there are low-interest rates for investors and relatively low risks.

P2P Lending Business Models

A p2p lending platform from any of the niches above can be realized according to two basic business models.

Three-parties company. In this case, there are three parties to the deal - the borrower, the lender, and the platform itself (represented by its creator).

Four parties company. According to the four-parties p2p business model, you have the participants mentioned above, plus a financial company that acts as a guarantor of debt repayment. In this case, there are lower interest rates for the investors (and lower risks) but higher interest rates for borrowers.

P2P Lending Platform Features

So, how to build a p2p lending platform? Let’s start with the essential features for both groups of users.

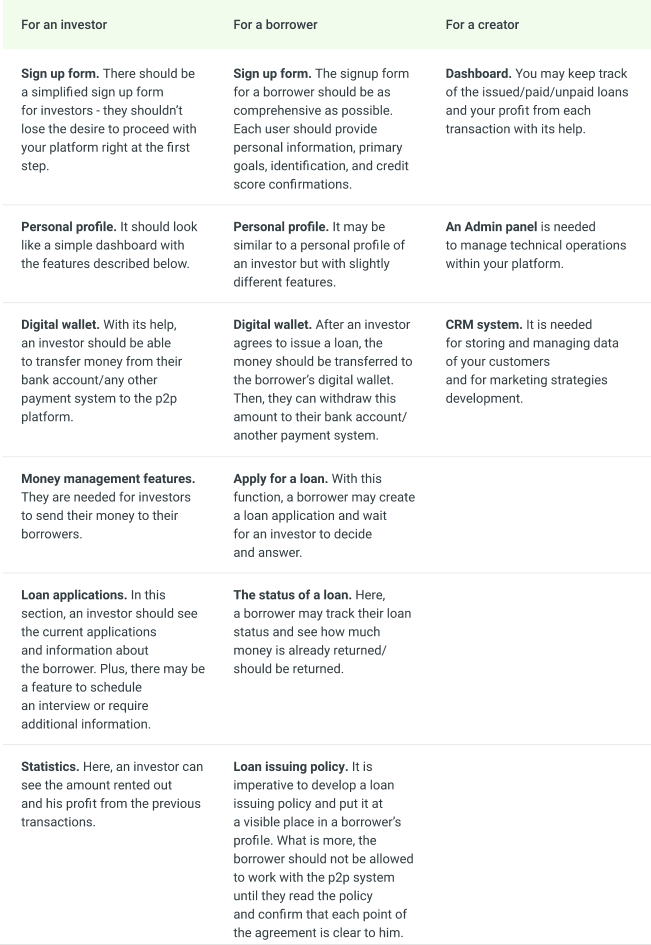

For an investor

Sign up form. There should be a simplified sign up form for investors - they shouldn’t lose the desire to proceed with your platform right at the first step.

Personal profile. It should look like a simple dashboard with the features described below.

Digital wallet. With its help, an investor should be able to transfer money from their bank account/any other payment system to the p2p platform.

Money management features. They are needed for investors to send their money to their borrowers.

Loan applications. In this section, an investor should see the current applications and information about the borrower. Plus, there may be a feature to schedule an interview or require additional information.

Statistics. Here, an investor can see the amount rented out and his profit from the previous transactions.

For a borrower

Sign up form. The signup form for a borrower should be as comprehensive as possible. Each user should provide personal information, primary goals, identification, and credit score confirmations.

Personal profile. It may be similar to a personal profile of an investor but with slightly different features.

Digital wallet. After an investor agrees to issue a loan, the money should be transferred to the borrower’s digital wallet. Then, they can withdraw this amount to their bank account/another payment system.

Apply for a loan. With this function, a borrower may create a loan application and wait for an investor to decide and answer.

The status of a loan. Here, a borrower may track their loan status and see how much money is already returned/should be returned.

Loan issuing policy. It is imperative to develop a loan issuing policy and put it at a visible place in a borrower's profile. What is more, the borrower should not be allowed to work with the p2p system until they read the policy and confirm that each point of the agreement is clear to him.

For a creator

Dashboard. You may keep track of the issued/paid/unpaid loans and your profit from each transaction with its help.

An Admin panel is needed to manage technical operations within your platform.

CRM system. It is needed for storing and managing data of your customers and for marketing strategies development.

Feel like you need competent help with a p2p platform development? You are at the right place!

Ask Us to Assist!How to Start a Peer to Peer Lending Business

Let’s proceed to the practical steps you need to undertake.

1. Decide on a niche

We’ve listed them for you, so feel free to choose the most appealing ones. What is more, don’t be limited to the niches above - you may develop something creative.

2. Checkup with the main laws

To do it right, make a clear decision about what users you're going to service. There are domestic and international laws in the field of finances, and you should comply with the both of them.

3. Research competitors

After your niche is determined, proceed with researching your competitors. For example, Lending Club helps borrowers with a bad credit history, while Funding Circle is good for small business financing. There are also lots of other locations, currency, and target customer-specific p2p lending websites you can research.

4. Develop an MVP

As you know, a Minimum Viable Product is essential for testing your business idea and developing the solutions to realize it. You may use our list of features to come up with a viable MVP to find out whether your target users are ready to use your solution.

5. Prove your concept

After testing your MVP, you will have many insights to prove whether your initial idea is really promising. Follow the initial path or adopt some changes but don’t forget to test each of your ideas one more time.

6. Proceed with the development

After you are sure that you are doing everything right, you may safely invest in a full-fledged product to launch into the fintech market.

How to Scale Your P2P Lending Business

Surely, you should create your peer to peer lending for a business startup with scaling and growth opportunities in mind. Here are high-end ideas you may realize after your p2p startup becomes demanded and popular.

Proceed with a mobile application

If you started by building a p2p lending website, creating a mobile application would be a worthwhile step. Modern users love mobile apps (you should always test this hypothesis even if you feel 100% sure). What is more, apps are more engaging. In the case of a p2p lending app, this means that your users will be able to invest and borrow money easier than ever.

Consider blockchain and smart contracts

If you didn’t initially make your p2p solution blockchain-based, you might fix this at any time. Protecting the data and transactions with blockchain infrastructure is one of the best ways to provide security. And with the help of smart contracts, each transaction becomes not only safe but also automatized.

Add AI-powered features

Artificial intelligence technology is especially useful when it comes to data analysis and decision making. Since the borrower should prove their solvency first, it will be more efficient to process this information with AI, especially if there are thousands of users, and their amount grows day by day.

Users will appreciate this feature. When a decision is made by artificial intelligence, there can be no human-made mistakes and biases.

This feature will also be useful for your investors since an AI-algorithm is good at evaluating risks and making reliable predictions about debt repayment.

Are There Some Limitations to Making a P2P Lending Platform?

How to start a p2p lending platform and avoid pitfalls? The right answer is to analyze them from the very beginning. Here are three main things to consider.

Legal compliance

Financial laws are very tricky in each country and each US state. There are many legal subtleties regarding the legal status of an enterprise that can provide online lending services, share capital, licenses, forms of taxation, and reporting. And since ignorance of the law is no excuse, you need to have a strong team of lawyers and financial advisors to complement your lending software development team.

The issue of trust

According to the Peer to Peer Lending Problems research, “P2P Lending does not only discuss between platforms and borrowers. We know that P2P Lending users are lenders. In this case, investment decisions are influenced by the lender's trust in the borrower and trust in the platform”.

How to establish this two-sided trust? The research above suggests paying the greatest attention to clarity, usability, the absence of hidden fees for both parties, design, security, and marketing. Well, it’s easier to say than to do.

The seamless repayment of a debt

Surely, you want the borrower to repay their debts according to the loan policy agreement. Also, you want your investors to easily agree to provide loans. However, force majeure is unavoidable on either side. To partially avoid them, you need to carefully check the borrower's solvency (AI is one of the best ways), and encourage investors to easily part with money, creating a risk-free and financially profitable space for everyone.

The cost to develop a p2p solution

The cost to develop a p2p platform will be individual regardless of the niche you choose. Most of the budget will be spent on developing functions to replenish the balance of the system and withdraw money to the borrower's account, payment integrations, and ensuring the safety of transactions and data within the system.

You will also have to spend money on researching user experience and developing custom and intuitive designs. The additional functions that we described above are another cost item. To invest wisely, just follow the Lean methodology, and carefully check the real need for each function or user interface element before investing in its creation.

Conclusion

It is much more challenging to understand the specifics of p2p lending, find your niche, and come up with a demanded idea than realize it technically. However, our professionals know how to approach both sides of the process wisely. With the help of business analysis and market research, we will find a bridge for your future solution developed by our technical team.

Want to learn more insider tips to p2p lending platform development?

Ask Us to Share!

Unit 1505 124 City Road, London, United Kingdom, EC1V 2NX

Unit 1505 124 City Road, London, United Kingdom, EC1V 2NX

Comments

Leave a comment